When an account owner disputes a payment with their bank, they must provide evidence to support their claim. In many cases, the bank’s goal is to protect their customer from having to pay for something they didn’t authorize or feel was misrepresented or damaged.

As the seller, you have the right to counter the account owner’s claim and provide evidence that supports your case. While Stripe doesn’t influence the ultimate outcome of the bank’s decision, our goal is to help you defend the dispute. We base the best practices that we provide here on our deep exposure to dispute resolution.

Likelihood of winning disputes

Your chances of overturning a dispute vary significantly based on several factors, including:

- The type of dispute and whether it qualifies for Visa CE 3.0 evidence

- The strength of the evidence you submit

- The type of payment (debit, credit, digital wallet, and so on)

- The type of purchase (online, in-person, physical product, service, and so on)

Stripe’s Radar for Fraud Teams uses Radar’s machine learning (ML) models to estimate your chances of winning a dispute. It gives you a prediction score in the dispute details page of your Dashboard, so you can prioritise disputes.

If you’re enrolled in Radar, but don’t see a win likelihood prediction next to a dispute, it’s likely one of the following reasons:

- The payment wasn’t made with a credit card

- The payment has only received an inquiry, not an actual dispute

- An error prevented us from generating a prediction (this is rare)

The prediction score ranks your likelihood of winning a dispute that you’ve submitted relevant evidence for from lowest (one dot) to highest (five dots). The following table shows the expected win percentage for each ranking. Even in the most favorable cases, it’s very difficult to overturn a disputed payment.

Keep your evidence relevant to the dispute reason and to the point

Card issuers review thousands of dispute responses every day. Writing a long explanation to them isn’t going to make your responses more convincing. Similarly, providing evidence about your clearly stated return policy isn’t relevant for a dispute claiming that the customer never received the product. Instead, describe clearly and concisely why the claim is unreasonable and how your evidence proves that, using a neutral and professional tone. For example:

Jenny Rosen purchased [product] from our company on [date] using a Visa credit card. We shipped the product on [date] to the address provided by the customer, and it was delivered on [date], as shown in the tracking file provided, so the claim that the product was not received isn’t true.

You can investigate the dispute while collecting evidence. For example, you can review Google Maps and Street View to see where your delivery took place, or check social media to help establish the customer as the legitimate cardholder.

Many businesses also include email correspondence or texts with their customer, but be aware that these exchanges don’t verify identity. If you include them, only include the relevant excerpts. For example, if you include a long email thread, redact any duplicated copy in the chain.

Keep your evidence factual, professional, and concise. Providing too little evidence is a problem, but overwhelming the card issuer with unnecessary content can obscure your argument.

Limit evidence file length

Card issuers manually review thousands of dispute responses daily and won’t comb through lengthy files to find the relevant argument for the network reason code.

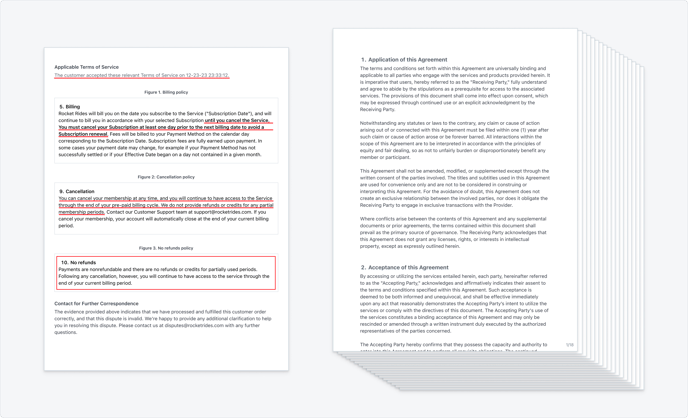

For example, if the dispute network reason code indicates “Cancelled Merchandise”, but the customer didn’t comply with your cancellation policy, don’t submit your entire Terms and Conditions agreement. Upload only the relevant cancellation policy section and use a callout or arrow to emphasise the details your customer violated.

- Do:

- Paste relevant excerpts from your terms into a single doc.

- Outline or underline text specific to the dispute type.

- Don’t:

- Upload your entire terms of service.

You can also decrease file size by:

- Reducing font size

- Single spacing documents

- Shrinking images within PDFs

The following information is essential for file types:

| EVIDENCE TYPE | RELEVANT DATA |

|---|---|

| Receipt | Date, currency, amount of disputed items |

| Shipping documentation | Delivery date and full shipping address |

| Cancellation policy or other Terms of service | Relevant subsections only |

| Customer communication | Customer name and relevant message |

Include proof of customer authorization

Fraudulent disputes account for over half of all disputes. It’s important to prove the legitimate cardholder was aware of and authorized the transaction in such cases. Any data that shows proof of this is a standard part of a compelling response, such as:

- AVS (Address Verification System) matches

- CVC (Card Verification Code) confirmations

- Signed receipts or contracts

- IP address that matches the cardholder’s verified billing address

Stripe always includes any AVS or CVC results along with the purchase IP address (if available from your Stripe integration). But if you have any other evidence of authorization (for example, 3DS authentication) include it too.

Include proof of service or delivery

After fraudulent disputes, other high frequency dispute reasons include claims from cardholders that products or services:

- Weren’t delivered

- Were defective or unsatisfactory

- Weren’t as described

Provide proof of service or delivery to refute such claims.

For a merchandise purchase, provide proof of shipment and delivery that includes the full delivery address, not just the city and postal code verification.

If your customer provides a “Ship to” name that differs from their own (for example, a gift purchase), be prepared to provide documentation explaining why they’re different. While it’s common practice to purchase and ship to an address that doesn’t match the verified billing address for the card, this is an additional dispute risk.

If your business provides digital goods, include evidence such as an IP address or system log proving the customer downloaded the content or used your software or service.

Include a copy of your terms of service and refund policy

When it comes to disputes, fine print matters. For returns or refunds, it’s critical to provide proof that your customer agreed to and understood your terms of service at checkout, or didn’t follow your policies. Include a clean screenshot of how you present your terms of service during checkout, with the relevant policy clearly emphasised.

Don’t, however, include the text of your entire policy, because card issuers won’t read through it all to find the relevant copy.

Combine files of the same evidence type

You must specify an evidence type for each file you upload, and you can only submit one piece of evidence per type. For example, you can combine several items representing communication with your customer (email messages, text screenshots, phone transcripts, and so on) into a single file for the Customer communication evidence. This also decreases your overall file length.

Formatting documents and images to upload

Include large, clear images for review. Whether you upload files through the Dashboard or the API, both have limitations on the acceptable file types and the combined file size.

- Only PDF, JPEG, or PNG file types are accepted

- The combined file size can’t be more than 4.5MB

- The combined page count must be less than 50 pages

- You can compress your files with tools such as Smallpdf

When submitting documents or images as evidence, use the following recommendations to make sure they can remain legible:

- Use a 12 point font or larger

- Make sure that documents are US Letter or A4 size, in portrait orientation (you can still add screenshots to your documents in landscape orientation)

- Use bold text, callouts, or arrows to draw attention to pertinent information

- Avoid using color highlighting

When uploading screenshots:

- Crop the screenshot to the area of interest and circle any key components (for example, delivery confirmation or signature)

- Use the text fields in the dispute evidence form to describe what the image contains and how it supports your response

The card issuer won’t review a response containing any illegible text or data.

Accepting disputes

You can accept a dispute, effectively agreeing that the cardholder’s reason for the dispute is valid. Accepting a dispute isn’t considered an admission of wrongdoing and is sometimes the most appropriate response. The customer has already received their refund through the dispute process – if you agree with the refund, it’s best to accept the dispute.

Take this action if you don’t intend to respond and submit evidence. Although accepting disputes doesn’t negatively affect your business any further, it’s not a viable alternative to an effective refund or returns policy. Dispute activity is calculated based on the disputes received, not won or lost, so dispute prevention is critical.

Note

Disputes incur a dispute fee that still applies if you accept the dispute.

Misunderstandings

For disputes that are the result of a misunderstanding, your customer can tell their card issuer that they no longer dispute the transaction. We recommend you still submit evidence to show that the payment was valid and to make sure the card issuer knows you’re not accepting the dispute.

In cases where you agree that the customer should keep the disputed funds, accept the dispute rather than ask the cardholder to withdraw the dispute for a regular refund. Remember, the card networks don’t consider how many disputes you win or lose, only how many you receive—a withdrawn dispute still counts as a dispute.

Disputes on partially refunded payments

While uncommon, a customer can dispute a payment for the full amount even if they’ve already received a partial refund (for example, a refund of a smaller amount that has been agreed upon). We understand this is frustrating as it amounts to an over-refund of more than the original purchase. Always respond in such cases because card issuers are very willing to rectify this situation.

Note

Because merchants can’t contest Cartes Bancaires disputes, you can’t ask the issuer to consider an existing partial refund when the full amount of a Cartes Bancaires payment is disputed.

Even if you plan to accept the un-refunded portion of the dispute, it’s important to provide evidence of the partial refund in your response. Include the amount and date of the refund, and even a screenshot of the refund information from your Dashboard (this is known as a “credit issued” response).

In most cases, the card issuer cancels the original dispute and then creates a separate one for the corrected amount. On Stripe, we use the existing dispute to track the overall outcome. If the dispute is fully resolved in your favor, you receive the entire amount back. If it’s not, you only receive the partially refunded amount. In this case, the dispute’s status is set to lost, and in the Dashboard, the dispute is marked as “partially won”.